The M-Pesa Moment for Kenyan Ecommerce Is Here — and It Looks Like NeoMali

Kenya built the world's most advanced mobile money system. M-Pesa let anyone send money instantly, without a bank account, without friction. It changed how East Africa moves value. But here is what M-Pesa never did: it never changed how Kenya sells. Until now. The M-Pesa moment for Kenyan ecommerce is here — and it looks like NeoMali.

Why M-Pesa changed payments — but not selling

When M-Pesa launched in 2007, it solved a problem every Kenyan already had: moving money safely and instantly. It did not ask people to become bankers. It met them where they were — on their phone, in their life. Today, M-Pesa processes over KES 2 trillion annually. It is table stakes for any Kenyan business.

But while M-Pesa perfected the payment, the selling side of the equation remained broken. Kenyan retailers — from the Gikomba wholesaler to the Eastleigh boutique owner to the WhatsApp-based boutique operator — were still running their businesses from WhatsApp group chats, Instagram DMs, and text message screenshots.

The gap M-Pesa left behind

Here is what that gap looks like in practice. A customer messages a seller on Instagram at 11 PM. The seller is asleep. The customer moves on. Or: a buyer sends a payment screenshot that turns out to be from a previous transaction. The seller ships the item. The money never arrives. Or: a shop owner calculates their daily sales by counting Till SMS messages manually — and still does not know what left their shelf.

These are not edge cases. They are the daily reality for millions of Kenyan retailers who are technically "online" but operationally running a business that cannot run without them in front of it 18 hours a day.

Enter NeoMali: the M-Pesa of selling

NeoMali was built to close that gap. The logic is identical to what Safaricom understood in 2007: the solution should not require users to become tech experts. The technology should adapt to how people already sell — not force them to rebuild their business from scratch.

NeoMali gives every Kenyan retailer two tools depending on how they operate:

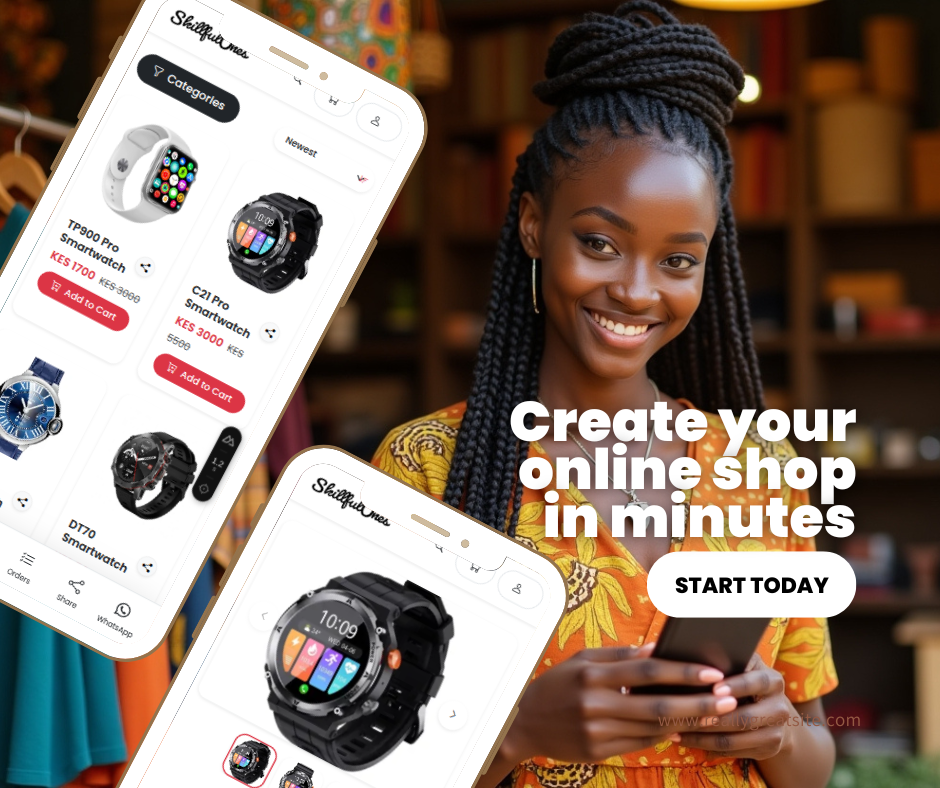

- NeoMali GO — for the digital hustler selling on Instagram, WhatsApp, and TikTok. A 24/7 online shop with M-Pesa STK Push checkout. Wake up to orders. No human required.

- NeoMali PRO-DUKA — for the duka commander with a physical shop. Real-time inventory sync between physical and online. Staff registers on their own phones. Stock leakage flagged automatically.

No credit card required. No technical degree needed.

Both products work the way M-Pesa works: you do not need to understand the infrastructure. You just need to sell. Setup takes under 5 minutes. There is no merchant account to negotiate, no payment gateway to integrate, no credit card to qualify for. M-Pesa STK Push is built in — the customer enters their PIN on their own phone, just like any M-Pesa transaction.

This is not a SaaS product built for Silicon Valley and adapted for Kenya. This is infrastructure built for how Kenyan retailers actually operate, priced at a level they can actually afford.

The category is being created right now

In 2007, there was no category called "mobile money." There was just cash, checks, and bank transfers. Safaricom did not enter an existing market — it created one. NeoMali is doing the same thing for Kenyan ecommerce. The retailers who understand this earliest will have the same advantage early M-Pesa adopters had: they grow into the category before it becomes crowded.

Just like M-Pesa changed how Kenya moves money, NeoMali is about to change how Kenya sells. The infrastructure is already paid for — M-Pesa proved Kenyan consumers will pay digitally. The only missing piece was a way for sellers to sell as easily as M-Pesa lets buyers pay.

That piece is NeoMali. And the moment is now.